Setting up a Business in Hong Kong

SUMMARY OF CONTENTS

PART A - INTRODUCTION

1 General

A foreign company wishing to carry on business in the Hong Kong Special

Administrative Region ("Hong Kong") may do so by either incorporating a Hong Kong

company (private company limited shares) )or registering a branch of that foreign company in Hong Kong. (The process

by which a Hong Kong company is set up is the same whether the incorporator is a

foreign company, a Hong Kong company, an individual or other legal entity.) The

relevant government authority is the Registrar of Companies (the "Registrar").

The purpose of this article is to assist our clients in setting up and maintaining a

business in Hong Kong through a Hong Kong (see Part B) or a foreign (see Part C)

company.

Some of the issues which arise in connection with doing business in Hong Kong, such

as registration with the taxation authorities and compliance with visa requirements,

involve similar considerations whether the business is to be operated as a separate

Hong Kong company or as a branch operation. These issues have accordingly been

dealt with generally (see Part A and Part F respectively).

Other issues, such as the method of registration of the relevant entity, differ greatly

depending on whether the client wishes to incorporate a Hong Kong company or

register a branch operation and have been dealt with separately. Accordingly, those

readers who are only interested in setting up a Hong Kong company need not refer to Part C and, likewise, those who have decided to set up a branch may disregard Part B.

2 Branch or subsidiary

The differences between a Hong Kong branch and a Hong Kong subsidiary of a

foreign company stem from the fact that, unlike a branch, a subsidiary is an entity

which, under Hong Kong law, is entirely separate from its parent. The business

activities available to a company in Hong Kong are generally not dependent upon

whether the company is locally incorporated and there is generally little practical

difference between operating a branch and a subsidiary company in respect of profit

computation. The rate of tax levied on profits is the same for local and foreign

companies and dividends are not subject to separate taxation in Hong Kong.

The usual reasons for preferring a subsidiary over a branch include the following:

(1) the parent company will not be liable for the debts of its subsidiary; its legal liability

will be limited to the amount of any unpaid issued share capital and its potential loss

will therefore be limited (in the absence of a guarantee or other security) to the value

of any assets it contributes by way of capital to the company

(2) only that information which relates to the subsidiary must be filed with the Registrar

and kept up to date

(3) a subsidiary does not need to file its accounts on the public record whereas in some

cases a foreign company will need to (see Part C)

(4) the presence of a branch in Hong Kong makes it more likely that the "parent"

company would be sued in Hong Kong even in connection with matters unrelated to

its business operations there

(5) it is usually simpler and more cost effective to set up a Hong Kong company than it is

a Hong Kong branch

(6) where the constitutional documentation in relation to the "parent" company is not in

English or Chinese, this will not require translation if a local company is incorporated,

whereas in the case of a branch it will require translation

(7) it is not necessary to arrange for certified copies of any documents to incorporate a

Hong Kong company whereas in the case of a branch it is so necessary

On the other hand, the usual reasons for preferring a branch over a subsidiary include

the following:

(1) there may be tax advantages under the tax laws of the place of incorporation of the

"parent", in particular, in relation to the treatment of any losses which the Hong Kong

operations may incur in the first few years of its operation

(2) a branch can often rely on the credit of the "parent" company

(3) if business operations are terminated in Hong Kong, the lengthy liquidation process

required for a Hong Kong company can be avoided and any capital can simply be

remitted out of Hong Kong

(4) a Hong Kong company can normally only reduce its issued capital with the consent of

the Court

(5) share repurchases by Hong Kong companies in some cases will require the consent

of the Court

(6) no stamp duty (except in relation to any land or any shares in Hong Kong companies

owned by the foreign company) will be payable on any transfer of the Hong Kong

business operated by a foreign company, whereas stamp duty will generally be

payable on any transfer of shares in a Hong Kong subsidiary company (see Part E)

(7) no duty is payable in Hong Kong on the authorised (or issued) share capital of a

foreign company with a Hong Kong registered branch

(8) the ongoing maintenance expenses involved with a branch can be lower than those

involved with a subsidiary, in particular, as Hong Kong law does not require the

separate audit of a branch

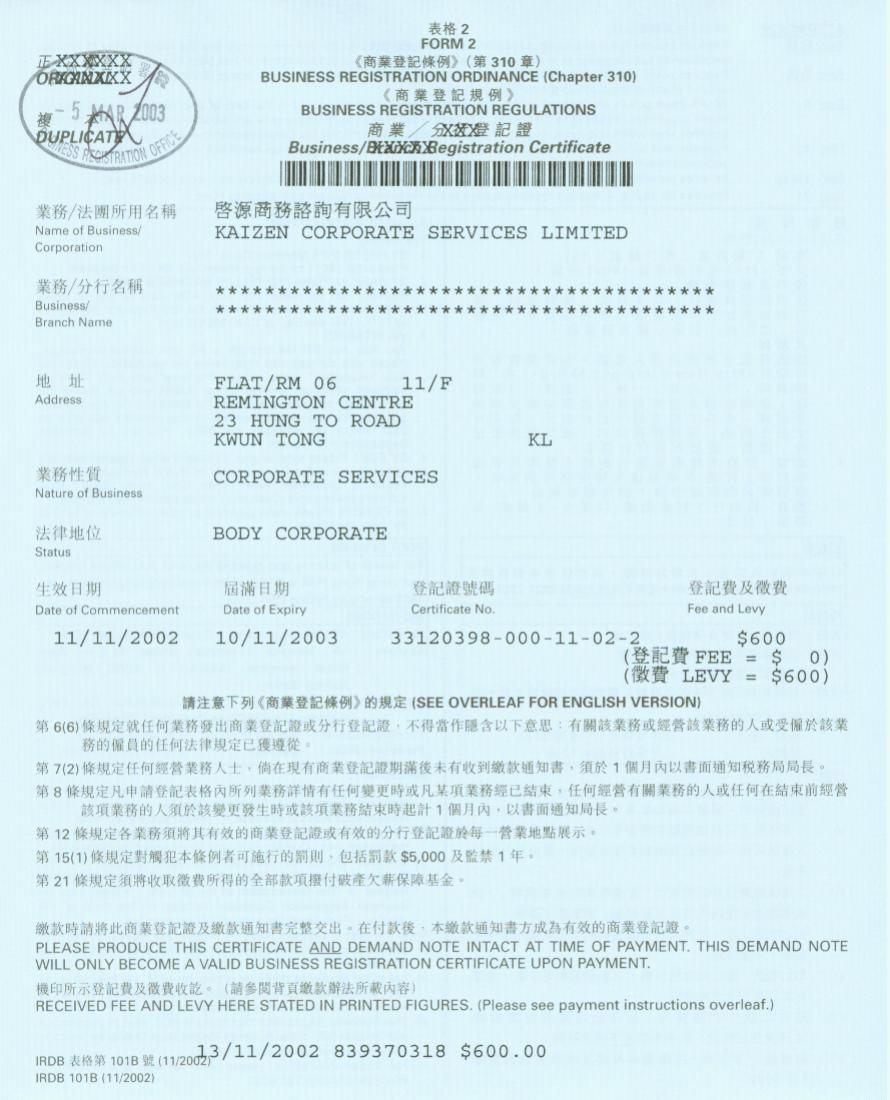

3 Business registration

The Hong Kong Business Registration Ordinance requires that every business in Hong Kong

register with the Business Registration Office. This is effected by the issuance of a

business registration certificate in respect of each location from which the business is

conducted. The certificate must be displayed on the premises. A business registration

certificate is valid for one year unless an election has been made for an expiry date of three years from the date of commencement endorsed on the certificate. The fee and

levy for the issue of the principal certificate is presently fixed at HK$2,600 per annum

and for each additional certificate HK$673 per annum. Normally, a new business

registration certificate can be issued immediately upon application and payment of the

required fee and levy. There is some relief for small business.

Registration with the Business Registration Office amounts to notification to the

Commissioner of Inland Revenue (the "Commissioner") that a business, which may be

subject to the payment of profits tax (see Part E), has been established.

It does not mean that any actual profits tax liability exists or is acknowledged.

All Hong Kong companies and foreign companies which have branches registered in

Hong Kong are deemed to be carrying on business in Hong Kong and must register

under the Business Registration Ordinance within one month of incorporation, even if

business operations have not yet commenced or within one month of having a place

of business in Hong Kong.

The particulars of the business must be briefly described in the application. The date

of commencement of business and, in the case of a company, the address of the

registered office (see Part B) or, in the case of a foreign company, the

authorised representative must

also be specified. A company which has adopted a Chinese name informally only (i.e.

it is not included in the company's Certificate of Incorporation or Certificate of Change

of Name) may also include this name in its application, but it is not necessary to do so.

The particulars registered with the Business Registration Office are available for

public inspection and any change in the registered particulars must be notified to the

Business Registration Office within one month.

4 Registration of charges

Both Hong Kong companies and foreign companies with Hong Kong branches (see Part C) must file (with the Registrar) the particulars of any registerable

charge:

(1) given by the company over its assets or

(2) existing over assets acquired by the company

normally within five weeks of the creation of the charge or the acquisition of such

assets, respectively.

Generally speaking, those charges requiring registration include floating charges and

charges over land, ships, goodwill, book debts, trademarks and patents and other

tangible assets. Foreign companies are only required to register charges over relevant

assets located in Hong Kong or which come into Hong Kong.

All companies are required to keep a register of charges over their assets (whether

they are registerable charges or not) containing short particulars of the assets

charged and the amount secured. In the case of foreign companies, this is limited to

assets located in Hong Kong or which come into Hong Kong. Further, all companies

are required to keep copies of registered charges. The register of charges must be

open for inspection by anyone whereas copies of registered charges are open for

inspection by members and creditors only.

Charges requiring registration which are not registered are generally void against a

liquidator of a company in a winding-up and against other creditors. For this reason a

person taking the benefit of a charge will usually take steps to ensure that the charge

is registered if it is required to be.

5 Additional licences and consents

Certain businesses may not be carried on in Hong Kong without a specific licence or

other consent to do so from the relevant regulatory authority, in addition to the

corporate requirements set out in this brochure. These businesses include banking,

deposit-taking, money-lending, securities and commodities dealing and advising,

leveraged foreign exchange trading and insurance.

A discussion of the relevant

requirements for these businesses is beyond the scope of this article but before

commencing to operate any such business, specific professional advice should be

obtained.

6 Prospectuses

The Companies Ordinance and the Securities Ordinance contain extensive provisions

in relation to the issue and distribution of prospectuses in Hong Kong concerning

shares in or debentures of companies, whether the company is registered in Hong

Kong or not.

Back to top

|

{kind=link}