Introduction to Corporate/LLC Income Tax in United States

According to 2017 Tax Cuts and Jobs Act, United States adopts combined worldwide taxation and new territorial-style tax system.

Worldwide taxation means income accruing in and outside of United States are subject to United State income tax. Under a worldwide tax system, secondary jurisdiction over foreign-source income exists. If the tax in the foreign country is lower than the tax rate in the residence country, residual tax will be imposed. If the tax rate in the foreign country is higher than the tax rate in the residence country, the corporate will pay the higher foreign tax rate and get a credit for foreign-source income in the future.

New territorial-style tax system means U.S. corporations that own 10% or more of a foreign corporation can take 100% dividend received deduction on dividends paid out of foreign-source earnings but cannot have foreign tax credit or deduction in this scenario. In addition, gain from the sale of stock in a foreign corporation is also eligible for the dividend received deduction. (The dividend received deduction is subject to a holding period requirement, which requires that the U.S. corporation held the foreign corporation stock for more than 365 days during the 731-day period beginning 365 days before the ex-dividend rate.)

There are two-type of business structures most popular in the United States: one is Corporate, the other one is Limited Liability Company (LLC), primarily because both minimize the owners personal liability. However, they have much differences regarding to taxation:

The Corporate is considered a separate legal entity, must file its tax return and pay income tax on its profits. This type of business can lead to double taxation?when the corporate makes profits and its owner(s) take all or part of profits out, because the corporate should file and pay income tax on the whole corporate profits and the owner(s) need to file and pay personal income tax on those take-out profits (called dividends). However, the corporate can choose not to pay dividends to its owner(s). In this scenario, no double taxation involved.

The LLC is considered a pass-through entity by default. This means that the business itself doesnt pay income taxes on its profits, while ALL the profits or loss are passed through to the owners (called members) and the members should add the profits or loss in his/hers/its personal income tax.

Keep in mind that the LLC can opt to be taxed as a corporation.

1.

|

U.S. Tax Resident

|

|

A corporation organised or created in the United States under the law of the United States or of any state is a domestic corporation. A domestic corporation is a resident corporation even though it does no business or owns no property in the United States. No other criteria related to place of management will cause a corporation to be domestic.

|

| 2. |

Federal Income Tax Rate

|

|

The corporate federal income tax rate is flat 21% for both U.S. tax resident and Non-U.S. tax resident companies. The corporate state income tax is different based on different states. There are 6 states dont impose state income tax: Nevada, South Dakota, Wyoming, Texas, Washington, and Ohio.

The LLC itself does not pay federal income tax, instead, the LLC members each pay taxes on their share of the profits on their personal (including individuals and entities) income tax returns. If the member(s) is/are individual, the federal income tax rate range from 10% to 37%, and the owner is also subject to self-employment tax with rate of 15.3%; if the member(s) is/are corporate, the federal income tax rate is flat 21%.

|

| 3. |

Withholding Tax Rate for Foreign Persons

|

|

Foreign persons doing business or non-business activities in the U.S. may subject to withholding tax. Please note that foreign persons include individuals and entities.

|

|

(1)

|

Business income: taxed on a NET basis with U.S. graduated rates.

Foreign persons shall be taxable on his/her/its taxable income which is effectively connected with the conduct of a trade or business with the U.S.. The gross income includes only gross income which is effectively connected with the conduct of trade or business within the U.S.

(a) Foreign individuals:

(b) Foreign corporations: Deductions shall be allowed only to the extent that they are connected with income which is effectively connected with the conduct of a trade or business within the U.S.

|

|

(2)

|

Non-business income: taxed on a GROSS basis with 30% statutory withholding rate, income tax treaties may apply.

The non-business income includes but not limited to interest, dividends, rents, salaries, wages, premiums, annuities, compensations, remunerations, emoluments, and other fixed or determinable annual or periodical gains, profits, and income.

(a) Foreign individuals: Non-resident alien individual present in the U.S. for 183 days or more during the taxable year, there is 30% income tax on the net gains from the sale or exchange of capital assets within the U.S.

(b) Foreign corporations: there is 30% income tax on gains from the sale or exchange of patents, copyrights, secret processes and formulas, goodwill, trademarks, trade brands, franchises, and other like property, to the extent such gains are from payments which are contingent on the productivity.

(c) Foreign corporations: repeal of tax on interest of foreign corporations received from certain portfolio debt investment.

|

4.

|

U.S.-Source Income

|

|

(1)

|

Income earned within U.S. borders is generally considered U.S.-source income.

|

|

(2)

|

Income earned within U.S. borders by a U.S. trade or business is U.S.-source income.

|

|

(3)

|

Dividends paid by a domestic corporation are U.S. source income.

|

|

(4)

|

Interest paid by a domestic corporation or the U.S. government is U.S. source income.

|

|

(5)

|

Royalties for the license of intangible property in the U.S., including patents and copyrights, would result in U.S. source royalty payments.

|

5.

|

Foreign-Source Income

|

|

(1)

|

Income earned outside U.S. borders is generally considered foreign-source income.

|

|

(2)

|

Income earned outside U.S. borders by a foreign trade or business is foreign-source income.

|

|

(3)

|

Dividends paid by a foreign corporation are foreign-source income.

|

|

(4)

|

Interest paid by a foreign corporation or a foreign government is foreign-source income.

|

|

(5)

|

Royalties for the license of intangible property in another jurisdiction, including patents and copyrights, would result in foreign-source royalty payments.

|

6.

|

Deductions (applicable to both Corporation and LLC)

|

|

Trade or business deductions are expenses that are attributable to the trade or business of the corporation are deductible. All of the ordinary and necessary expenses paid or incurred during the taxable year in caring on a business are deductible.

|

|

(1)

|

Bad Debt

Under accrual-method taxpayers must use direct write-off method for tax purposes.

|

|

(2)

|

Business Interest Expense

For general-business interest expense, all interest paid or accrued during the taxable year on indebtedness incurred for business purposes is limited to the sum of:

(a) business interest income;

(b) 30% of adjusted taxable income of the taxpayer for the taxable year; and

(c) the floor plan financing interest of the taxpayer.

Exceptions to the 30% limitation apply to real property and farming business, and any taxpayer whose average annual gross receipts in the three preceding years do not exceed $25 million.

For interest expense on loans for investment, it is limited to net investment income.

|

|

(3)

|

Organizational Expenditure and Start-up Costs

The corporation may elect to deduct up to $5,000 of organizational expenditures and $5,000 of start-up costs. Each $5,000 is reduced by the amount by which the organizational expenditures or start-up costs exceeds $50,000 respectively. Any excess organizational expenditures or start-up costs are amortized over 180 months.

|

|

(4)

|

Organizational Expenditure and Start-up Costs

The corporation may elect to deduct up to $5,000 of organizational expenditures and $5,000 of start-up costs. Each $5,000 is reduced by the amount by which the organizational expenditures or start-up costs exceeds $50,000 respectively. Any excess organizational expenditures or start-up costs are amortized over 180 months.

|

|

(5)

|

Business Meals and Entertainment

Business meals are 50% deductible to the corporation. Business entertainment is no longer deductible.

|

|

(6)

|

Business Gift

Business gifts are deductible up to a maximum deduction of $25/recipient/year.

|

|

(7)

|

Life Insurance Premiums

If the premiums are paid on policies where the beneficiary is named by the insured employee, such premiums are deductible as an employee benefit.

|

|

(8)

|

Executive compensation

A publicly held corporation may not deduct compensation expenses in excess of $1,000,000 paid to the CEO/CFO

|

|

(9)

|

Casualty Losses

Generally, any losses not compensated by insurance or otherwise is deductible.

|

|

(10)

|

Charitable Contributions

Corporations making contributions to recognized charitable organizations are allowed a maximum deduction of 10% of their taxable income.

Any disallowed charitable contribution may be carried forward for 5 years.

The taxable income is calculated before the deduction of:

(a) Any charitable contribution deduction;

(b) Dividend received deduction;

(c) Any capital loss carry back.

|

|

(11)

|

Capital Losses/Gains

The corporation capital losses can only offset capital gains but cannot deduct other business income.

Net capital losses are carried back 3 years and forward 5 years and are applied only against capital gains.

|

|

(12)

|

Net Operating Losses

The corporation net operating losses can only be limited to 80% of taxable income.

Net operating losses may be carried forward indefinitely.

|

|

(13)

|

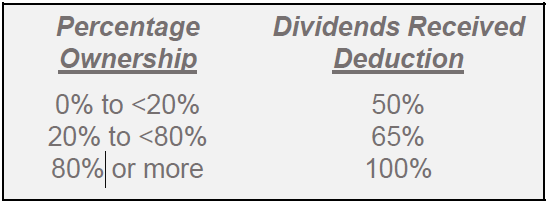

Dividend Received Deduction (applicable only to Corporation)

To avoid triple taxation of earnings, the amount of the dividends received deduction allowed is dependent upon the percentage of the investee corporation owner by the investor corporation.

Requirements: The corporate shareholder must own the investee stock for more than 45 days during the 91-day period beginning on the date 45 days before the ex-dividend date of the stock. Below are the percentage deductions based upon stock ownership:

The dividend received deduction (DRD) equals the lesser of:

(a) 50%/65% dividends received, or

(b) 50%/65% of taxable income, which is computed without regard to DRD, any net operating loss deduction, or capital loss carry back.

|

|

NOTE: DRD does not apply to Personal Service Corporations, Personal Holding Companies, and S Corporations.

|

7.

|

Compliance

|

|

(1)

|

Corporations are required to pay estimated taxes when their expected tax liability (income tax due) for the tax year exceeds $500. Corporation should file income tax return before April 15th each year (under Calendar year).

|

|

(2)

|

The first step in computing estimated tax is to determine the Required Annual Payment, which is LESSER of:

(a) 100% of the tax on the current years income tax return; or

(b) 100% of the tax of the prior years income tax return.

|

|

(3)

|

Each estimated tax (equal to 25% of the Required Annual Payment) are made in quarterly instalments due by the 15th day of the 4th, 6th, 9th, and 12th months of the corporations tax year.

For example, if a corporate adopt calendar to file tax return, the instalment schedule are as follows:

|

|

Calendar Year

|

|

1st Quarter Instalment

|

April 15th

|

|

2st Quarter Instalment

|

June 15th

|

|

3st Quarter Instalment

|

September 15th

|

|

4st Quarter Instalment

|

December 15th

|

|

|

(4)

|

Estimated Tax Underpayment Penalty

(a) The amount subject to penalty is equal to the difference between the required instalment and the actual amount paid. This difference is calculated for each of the instalments due during the year.

(b) The period of underpayment runs from the due date of the instalment to the date the underpayment is rectified or the due date of the tax return, whichever coms earlier.

(c) The penalty rate is equal to the Federal short-term rate plus 3%, or add 5% for underpayments in excess of $100,000.

|

8.

|

Information Return with Respect to Certain Foreign Corporation (Form 5471)

|

|

(1)

|

Form 5471 is required to be filed if your company meets one of the following scenarios:

(a) U.S. company who owns (directly, indirectly, or constructively) 10% or more of the total voting power/stock of a foreign corporation at any time during any tax year.

(b) U.S. company who is an officer or director of a foreign corporation in which any U.S. company or person has acquired 10% stock ownership.

(c) U.S. company who acquired additional stock to meet the 10% stock ownership requirement or disposed of stock in a foreign corporation to reduce their ownership below the 10% stock ownership requirement. The acquisition or disposition of stock detailed information need to be disclosed on Form5471.

U.S. company mentioned above includes:

(a) A domestic partnership,

(b) A domestic corporation, and

(c) An estate or trust that is not a foreign estate or trust.

|

|

(2)

|

The identity information of the U.S. company and the foreign corporation is required to be disclosed on Form 5471 for all the taxpayers. Some other schedules are required depends on how much ownership of the foreign corporation is held by the U.S. company. For example, for U.S. person having more than 50% ownership (by voting power or total value of stocks) in a foreign corporation during the annual accounting period of the foreign corporation, the following information are necessary:

(a) Stock of the foreign corporation: including the total number of shares and the number of shares held by the U.S. shareholders and direct shareholders.

(b) Balance sheet and Income Statement of the foreign corporation presented with U.S. dollars.

(c) General information to describe the foreign corporation.

(d) The U.S. companys pro rata share of income from the foreign corporation.

(e) Transactions between the foreign corporation and the U.S. company.

(f) Transactions between the foreign corporation and other controlled participants.

|

|

(3)

|

Attach Form 5471 to the companys income tax return and file both by the due date (including extensions) of the companys business tax return. Failure to file information required on Form 5471 and schedule forms is subject to the following penalties:

(a) A $10,000 penalty is imposed for each annual accounting period of each foreign corporation.

(b) If the information is not filed within 90 days after the IRS has mailed a notice of the failure to the U.S. person, an additional $10,000 penalty (per foreign corporation) is charged for each 30-day period, or fraction thereof, during which the failure continues after the 90-day period has expired. The additional penalty is limited to a maximum of $50,000 for each failure.

(c) Criminal penalties may apply.

|

9.

|

Information Return of 25% Foreign-Owned U.S. Corporation or a Foreign Corporation Engaged in a U.S. Trade or Business (Form 5472)

|

|

Form 5472 is used for a reporting corporation to provide information required under sections 6038A and 6038C when reportable transactions occur with a foreign or domestic related party.

|

|

(1)

|

Reporting corporation is either a 25% foreign-owned U.S. corporation or a foreign corporation engaged in a trade or business within the United States. A corporation is 25% foreign owned if it has at least one direct or indirect 25% foreign shareholder (via the total voting power or total value of stocks of the corporation) at any time during the tax year.

|

|

(2)

|

Related party is broadly defined to cover:

(a) Any direct or indirect 25% foreign shareholder of the reporting corporation;

(b) Any person or business entity who is related to the reporting corporation according to special ownership-attribution rules;

(c) Any person or business entity who is related to a 25% foreign shareholder of the reporting corporation according to special ownership-attribution rules;

(d) Any entity that is owned or controlled by the same persons as the reporting corporation pursuant to the transfer-pricing rules.

|

|

(3)

|

Reportable transaction is any type of transactions listed on Form 5472 which is very broadly defined. Basically, it includes any type of activity between a foreign related party and the US corporation, with no limit in value. A reportable transaction does not include the payment of dividends. There are some examples of reportable transactions:

(a) The exchange of money or property, including payments, rental income, sales transactions, remuneration, commission payments, capital contributions and capital reductions.

(b) The use of US company property, such as real estate, by a foreign owner or related party.

(c) Loans and/or interest payments between the corporation and a foreign owner.

|

|

(4)

|

Form 5472 usually requires the following information with regard to the reporting corporation, 25% foreign shareholder, and the related party:

(a) The name, address, and U.S. taxpayer identification number (if applicable);

(b) The nature of business and the principal place or places where conducts its business;

(c) Each country in which they file income tax returns as a resident under the tax laws of that country;

(d) The relationship of the reporting corporation to the related party;

(e) The nature and amount of the reportable transactions with the foreign related party.

|

|

(5)

|

File Form 5472 as an attachment to the reporting corporations income tax return by the due date (including extensions) of that return. Failure to file a Form 5472 or maintain the supporting records as required could result in the following penalties:

(a) A penalty of $25,000 will be assessed on any reporting corporation.

(b) If the failure continues for more than 90 days after notification by the IRS, an additional penalty of $25,000 will apply. This penalty applies with respect to each related party for which a failure occurs for each 30-day period (or part of a 30-day period) during which the failure continues after the 90-day period ends.

(c) Criminal penalties may apply for failure to submit information or for filing false or fraudulent information.

|

See also:

Our US Comapny Formation Services

Open U.S. Business Bank Account Remotely (For Companies Registered by Kaizen)

Open U.S. Business Bank Account Remotely (For Existing Company)

Our US Auditing Services

Our US Book-keeping and Accounting Services

Our US Auditing Services

USA Trademark Registration Costs and Procedures (2020)

|